How Much Did U.S. Semiconductor Export Controls Accelerate China’s Push for Self-Sufficiency?

In terms of Chinese government subsidies, not at all.

A few weeks ago, a former very senior U.S. government official asked me a question:

“So how much do you think semiconductor export controls contributed to China’s push for self-sufficiency? It can’t be zero, right?”

It definitely isn’t zero, but the size, contribution, and timing of the effect are different than the most vocal critics of export controls claim. Get the answer to this question wrong and you get the policy wrong. This includes, urgently, the policy this administration is now deciding in the wake of Donald Trump’s trip to China, with Nvidia CEO Jensen Huang riding along.

Ming-yen Ho is a non-resident fellow at a Taiwanese think tank, the Research Institute for Democracy, Society, and Emerging Technology (DSET). Last year, Ho published a paper on China’s semiconductor industry. Among many other virtues, the paper provides an interesting dataset to apply to the export controls question. Specifically, Ho has published the best dataset that I have seen thus far on how much the Chinese government is putting into semiconductor industry subsidies and equity investments (which have many of the same effects as subsidies). He also obtained good data on how much investment Chinese semiconductor firms are receiving each year from foreign investors, which can shed some light on how they responded to the controls.

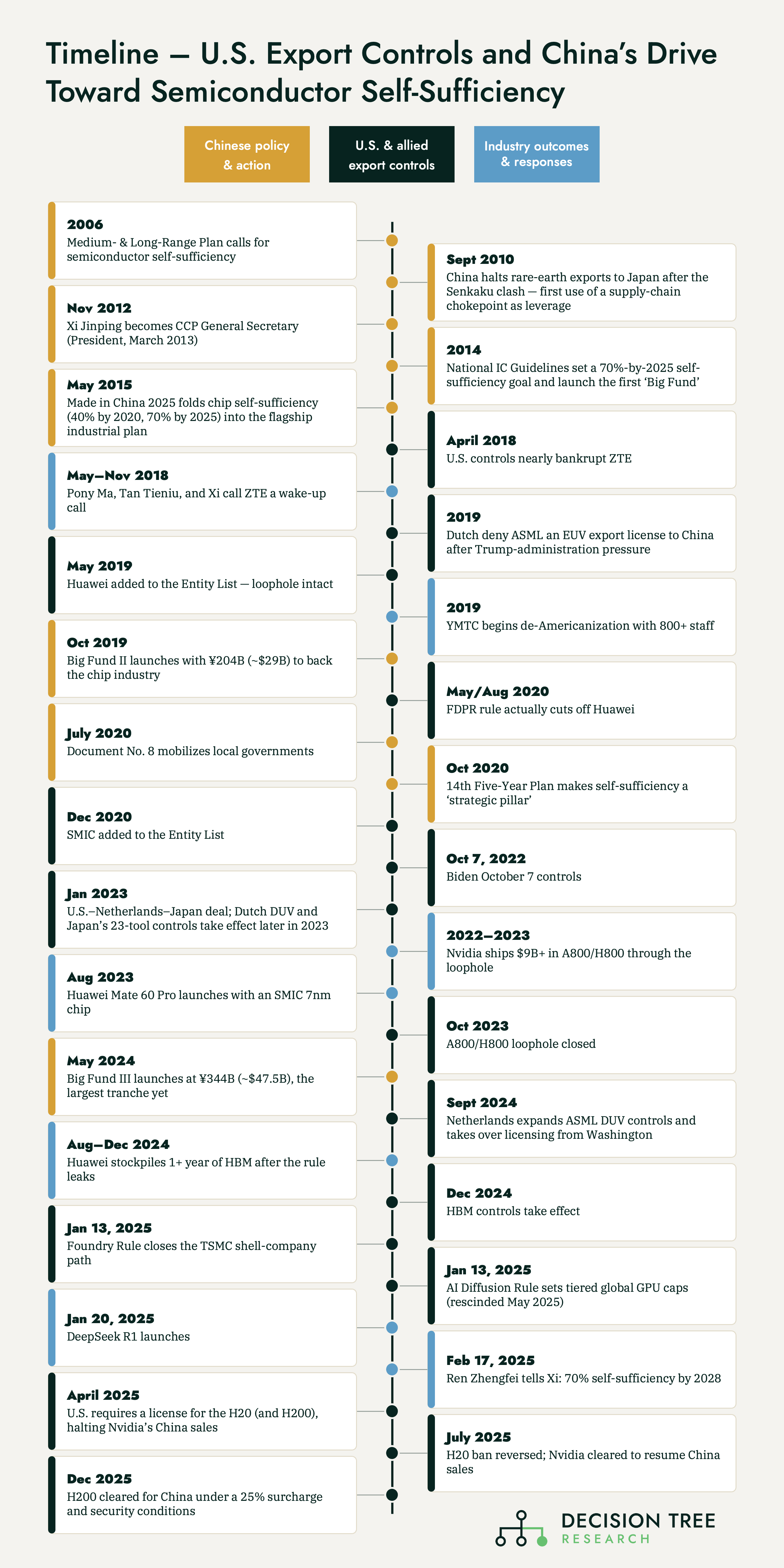

If we compare Ho’s dataset to the timeline of the biggest events in U.S. semiconductor export controls and Chinese semiconductor industrial policy, we can test the hypothesis that U.S. export controls led to a big spike in Chinese government support to the industry. While government subsidies are not the only Chinese reaction that should interest U.S. policymakers, they’re still a hugely relevant test case. A mostly complete timeline of key export control events is included at the end of this article. But for our purposes, there are three events that loom largest:

Made in China 2025, the 2015 policy in which China made semiconductor self-sufficiency a core goal of its industrial policy;

The 2018 ZTE export controls, which were the first big semiconductor move by the first Trump administration; and

The October 7, 2022 export controls by the Biden administration on AI and semiconductor tech.

As you review the subsidy and investment data, keep two things in mind:

Causality can’t run backwards in time: export controls cannot cause trends that existed before the export controls do (or at least before the perceived threat exists).

The change in the trend matters more than the change in the values: An observation that China’s investment in self-sufficiency is increasing or decreasing after the export controls doesn’t by itself tell us that the export controls had an effect. We need to know whether the rate of increase or decrease has changed. Knowing the change in trend helps us understand the difference between where China is now and where China would have been in an alternative scenario in which the export controls were never applied (what historians and social scientists refer to as the counterfactual analysis).

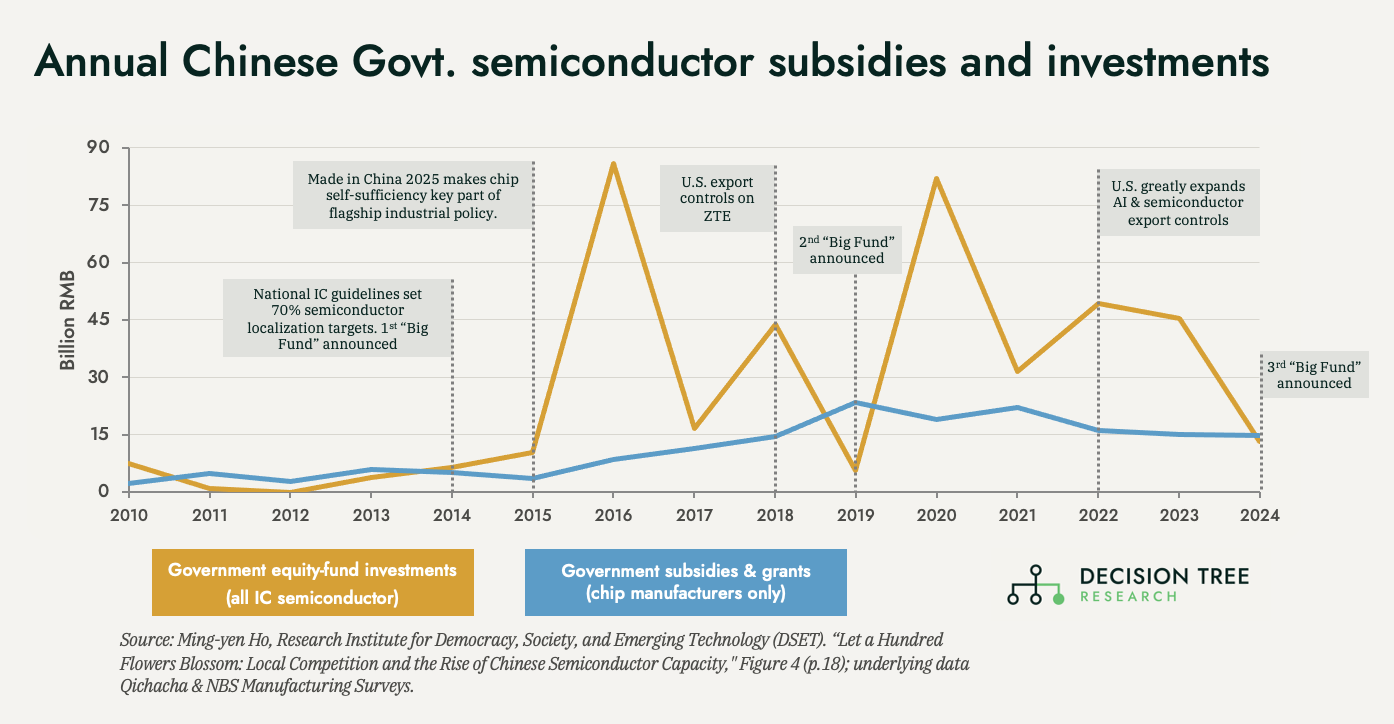

Chinese semiconductor self-sufficiency has been a stated goal of Chinese policy for decades, long preceding the modern U.S. approach to export controls that began in 2018. Moreover, this is not merely a goal, but one that the Chinese government has been willing to invest enormous amounts of money in. The river of money began with the first “Big Fund” in 2014, when the Chinese government started pouring tens of billions of dollars’ worth of investment into the semiconductor industry. The first Big Fund ended up being about $21 billion of investment, and was followed by a ~$29 billion second Big Fund in 2019 and a ~$48 billion third Big Fund in 2024. The first Big Fund was paired with a simultaneous dramatic expansion of the subsidies available to chipmakers, though the second and third weren’t.

Now let’s take a look at the data itself.

Looking at the timeline, there are two big investment spikes, in 2016—after Made in China 2025 and the first “Big Fund” of government semiconductor equity investments got underway in earnest—and again in 2020, after the second Big Fund was announced. When 2025 and 2026 data is available, it will likely show another spike reflecting investments by the third Big Fund, which was announced in 2024.

Based on the explanations given by Chinese policymakers and documents at the time (which expressed fear of dependence on the U.S.), it is at a minimum plausible that the 2018 ZTE export controls caused the spike in 2020. However, the government subsidy and investment levels were broadly similar to those present before the export controls.

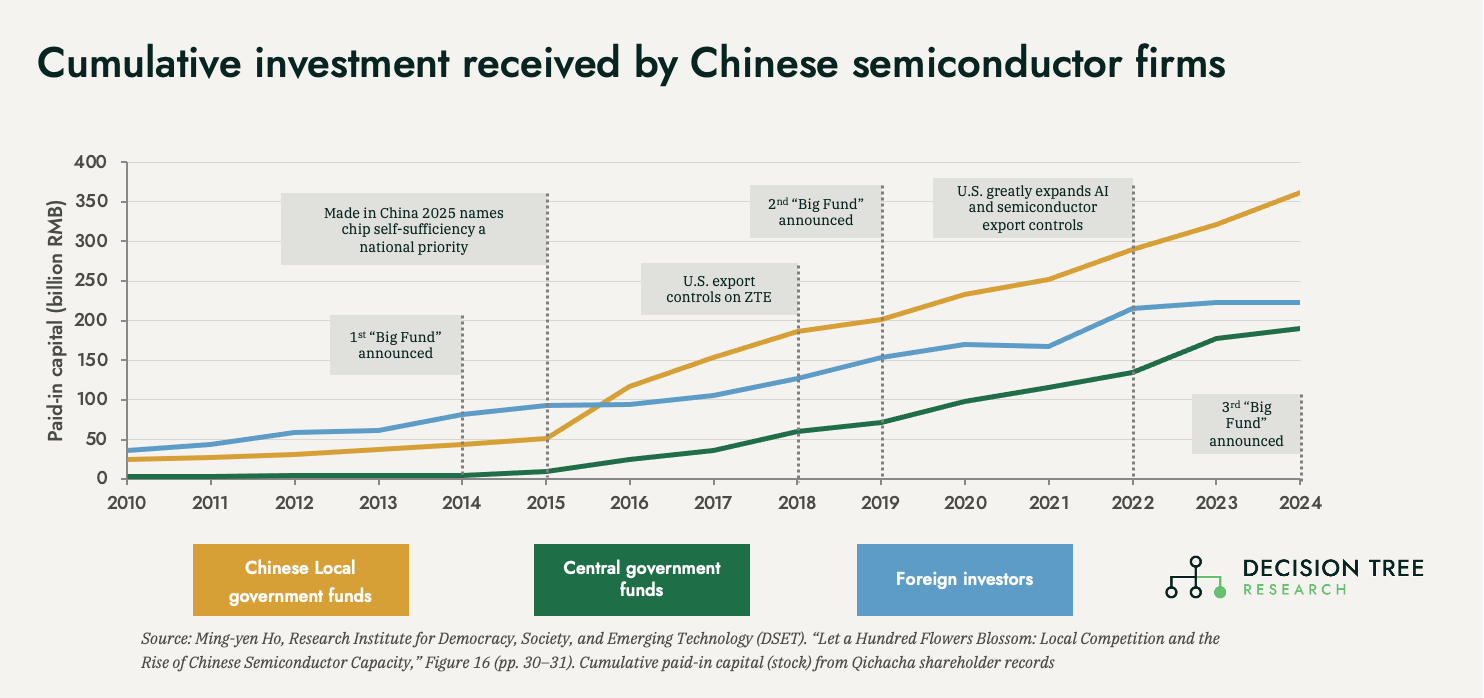

The “this is just the continuation of the previous trend” explanation is even more obvious when you look at the government equity investments received by Chinese companies in the form of paid-in capital stock. Again, government equity investments are a very important tool of Chinese semiconductor industrial policy. In terms of their impact, government equity investments are similar to direct subsidies.

The Big Funds used large single-year government outlays to establish the investment vehicles themselves (hence the big spikes), but those financial resources are disbursed to semiconductor companies at a more consistent rate over time. The second Big Fund was evidently established when the first one ran out of money with the goal of continuing the same rate of industry investment, not increasing the level as a response to export controls.

Thus, the Chinese government’s overall rate of accumulation of semiconductor equity ownership investment was almost unchanged in the period after the ZTE export controls. After the 2022 Biden export controls, the rate of government investment actually decreased a bit. China’s semiconductor industry’s access to foreign private sector capital investment dropped to almost zero in the wake of the controls, which makes sense as a reaction to the new U.S. policy.

In short, available data on Chinese government subsidies and equity investment does not provide strong support for the hypothesis that export controls were a deciding factor in the Chinese government’s decisions about the appropriate level of investment.

My favored interpretation of the data is that, in 2018, the government had already reached or exceeded what it perceived to be the maximum productive rate of subsidization in pursuit of its previously decided policy of self-sufficiency. After all, the first billion dollars of subsidization (from 0 to 1) helps a lot. The 100th billion dollars (from 99 to 100) helps far less. At a certain point, all the additional subsidization and investment doesn’t buy you a more robust semiconductor industry: it just fuels further corruption and waste. The first Big Fund already had corruption and waste in abundance.

Perhaps the Chinese government would have liked to subsidize and invest more if it had additional attractive options available, but those options did not seem to exist. The exodus of foreign capital probably made things worse, since interest by sophisticated foreign investors can help provide persuasive evidence to not always especially sophisticated Chinese government bureaucrats that a given Chinese company has real merit and is not merely a scam.

Government investment is not the only data that we’re interested in to answer this question, and in a future post, I’ll share some additional interesting data on the change in China’s chip sales, chip production capacity, and the rate of technological progress of China’s leading chipmakers.

So let’s return to the question from the former senior U.S. policymaker:

“How much do you think semiconductor export controls contributed to China’s push for self-sufficiency? It can’t be zero, right?”

Actually, it might be zero, at least in terms of government investment in the semiconductor industry.

Of course, the Chinese government has other tools to achieve its goals besides subsidies—facilitated smuggling, state-backed industrial espionage, coercion of international firms, stockpiling of manufacturing equipment, etc.

And the Chinese government is not the only relevant actor: the Chinese memory chipmaker YMTC launched a very large and well-resourced de-Americanization campaign in 2019 that was clearly a response to U.S. export controls on ZTE and Huawei and the fear that YMTC would be next.

But for Chinese government investing and subsidies specifically, export controls do not seem to have moved the needle. Made in China 2025 had already directed the government to do everything in terms of investing and subsidizing that it could. By 2022, that had been true for nearly a decade.